The Moment of Truth Is Approaching

The Moment of Truth Is Approaching

This is a thorough overview, so please refresh your beverage of choice.

We are approaching a financial-economic Moment of Truth that confirms that either 1) "the status quo is unchanged and will continue on the same path"--employment will be strong, inflation and interest rates will decline ("the soft landing"), profits will continue to rise and all will be right with stocks, housing, consumer spending and the global economy--or

2) fundamental changes are occurring beneath the surface that will destabilize a great many things we currently take for granted: the permanence of low unemployment, inflation and interest rates, and of course soaring profits, housing and stock market valuations.

This is a thorough overview, so please refresh your beverage of choice.

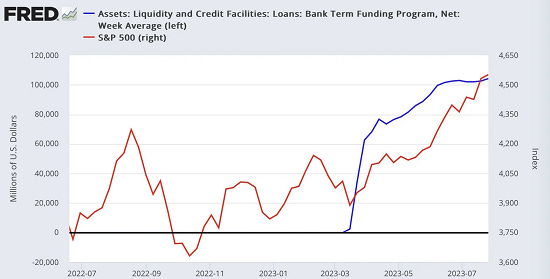

In broad brush, here's what happened the past year: to tamp down inflation, the Federal Reserve raised bond yields/interest rates at the fastest rate in decades. These higher interest rates broke the stable earnings of many medium-sized banks, which then saw capital flowing from banks to money-market funds that paid much higher yields on cash.

On March 10 2023, Silicon Valley Bank collapsed, and the Fed rushed to create a new fund to ease access to credit, the Bank Term Funding Program (BTFP). As this chart shows, the fund quickly expanded to $100 billion (blue line), which then sparked a massive stock market rally (red line) as this new liquidity immediately boosted equities. Euphoria over the profit potential of AI and rising confidence in "the soft landing"/ no recession added bullish fuel to the rally.

The banking crisis appears to have been resolved, but the higher interest rates have changed the flow of capital and the profitability of banks. The stability created by the flood of Fed liquidity may well be temporary.

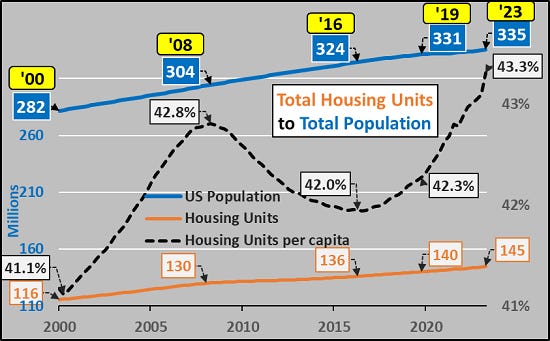

Concurrently, the rise in interest rates doubled mortgage rates from the 3% range to the 6% to 7% range while housing valuations skyrocketed, supposedly due to scarcity. Statistically, the number of housing units per capita (per person) in the US has never been higher, so it seems the demand outstripped supply for financial reasons, what my colleague CH calls an "interest rate driven, credit deluge bubble."

I also see the massive corporate buying of houses for rentals and individual-investor mass-market buying of dwellings to cash in on the AirBNB boom (that's now drying up) as major sources of housing demand that were largely driven by (pandemic-generated) excessively low rates and easy credit.

Recall that buyers are motivated to "buy now rather than later" as mortgage rates start to rise to lock in a rate before they move even higher.

The consensus holds that the Fed will soon start lowering interest rates back to zero as inflation falls back to the 2% annual target. (So our money only loses 22% of its purchasing power every decade, and that's "low inflation"?)

Many (myself included) have made the case for systemically higher inflation due to global scarcities, higher costs of resource extraction, deglobalization, labor shortages, re-industrialization and the decay and reversal of financialization, i.e. the stupendous expansion of credit, leverage and commoditized global financial instruments.

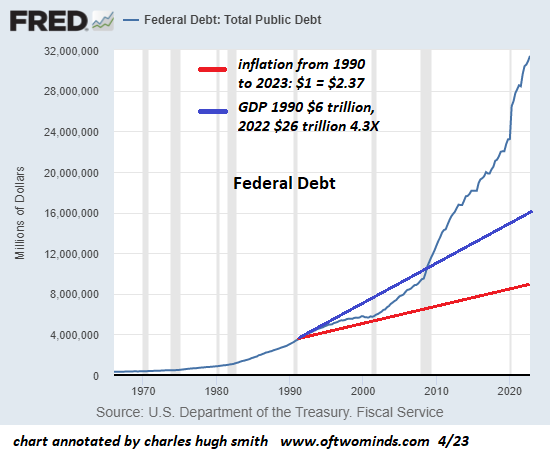

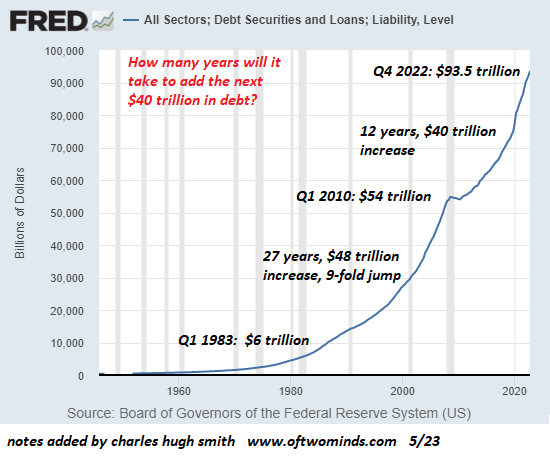

Meanwhile, the Federal government, corporations and state and local governments, have been borrowing money at rates that have reached parabolic heights.

This unprecedented expansion of federal debt outside of war or recession triggered a downgrade of the federal credit rating.

The "risk" in Treasuries isn't default of course, as they can create money (or borrow it into existence via the Fed) to pay the interest; the risk is inflation driven by all that money-creation. In a deflationary economy like Japan, the inflationary money-printing to buy government bonds offsets the "real economy's" deflation. In an inflationary economy, this "self-funding of debt" via creating money to fund soaring government debt will drive inflation higher.

Keep reading with a 7-day free trial

Subscribe to Charles Hugh Smith's Substack to keep reading this post and get 7 days of free access to the full post archives.